The Power of a Millionaire Mindset.

Having a Millionaire Mindset is the key to financial success. The way you think about money affects how money is earned, saved, and invested. Millionaires don’t just work for money! they make money work for them!

Many believe wealth comes from luck or high paying jobs, but it’s really about mindset and habits. Wealthy people focus on long-term financial growth, not just quick paychecks. They know that small, smart money moves add up over time.

Changing how you think about money can help you escape financial struggles and build real wealth. Learning about assets and liabilities is a game changer. When you start thinking like a millionaire, you make choices that lead to lasting success.

Success Starts with the Right Millionaire Mindset! Millionaires Think Differently About Money…

A Millionaire Mindset starts with how you see money. Most people think of money as something to earn and spend. Millionaires see it as a tool to create more opportunities. They focus on long-term security instead of short-term pleasures.

Instead of working just to pay bills, millionaires make smart financial decisions. They avoid impulse spending and invest their money wisely. Every dollar has a purpose! whether it’s for growing wealth, security, or reinvestment.

Thinking differently about money puts you in control of your financial future. Instead of getting stuck in a cycle of earning and spending, focus on earning and investing. Even small financial changes can lead to big long term success.

The Difference Between Working for Money Versus Making Money Work for You.

Most people trade time for money. They work hard for every dollar they earn. If they stop working, their income stops too. This cycle keeps them dependent on a paycheck.

A Millionaire Mindset changes that. Wealthy people don’t just work for money! They make money work for them. They invest in assets that generate income. Their money keeps growing, even when they aren’t working.

By shifting from earning paychecks to building income streams, you create financial freedom. The goal is to set up systems that let your money grow on its own. This gives you more control over your time and future.

Shifting from Paycheck Dependency to Long-Term Wealth Building.

Living paycheck to paycheck is stressful. It leaves no room for savings or investments. When all your money goes to bills, it’s hard to think about long term wealth. Breaking this cycle starts with changing your mindset.

A Millionaire focuses on wealth building instead of short term spending. Instead of using every paycheck for bills and luxuries, millionaires set aside money for investments. They know financial freedom comes from growing money, not just earning it.

Start small! Save automatically, invest in assets, and cut unnecessary expenses. These small habits add up over time. Wealth isn’t built overnight, but smart choices lead to long-term financial security.

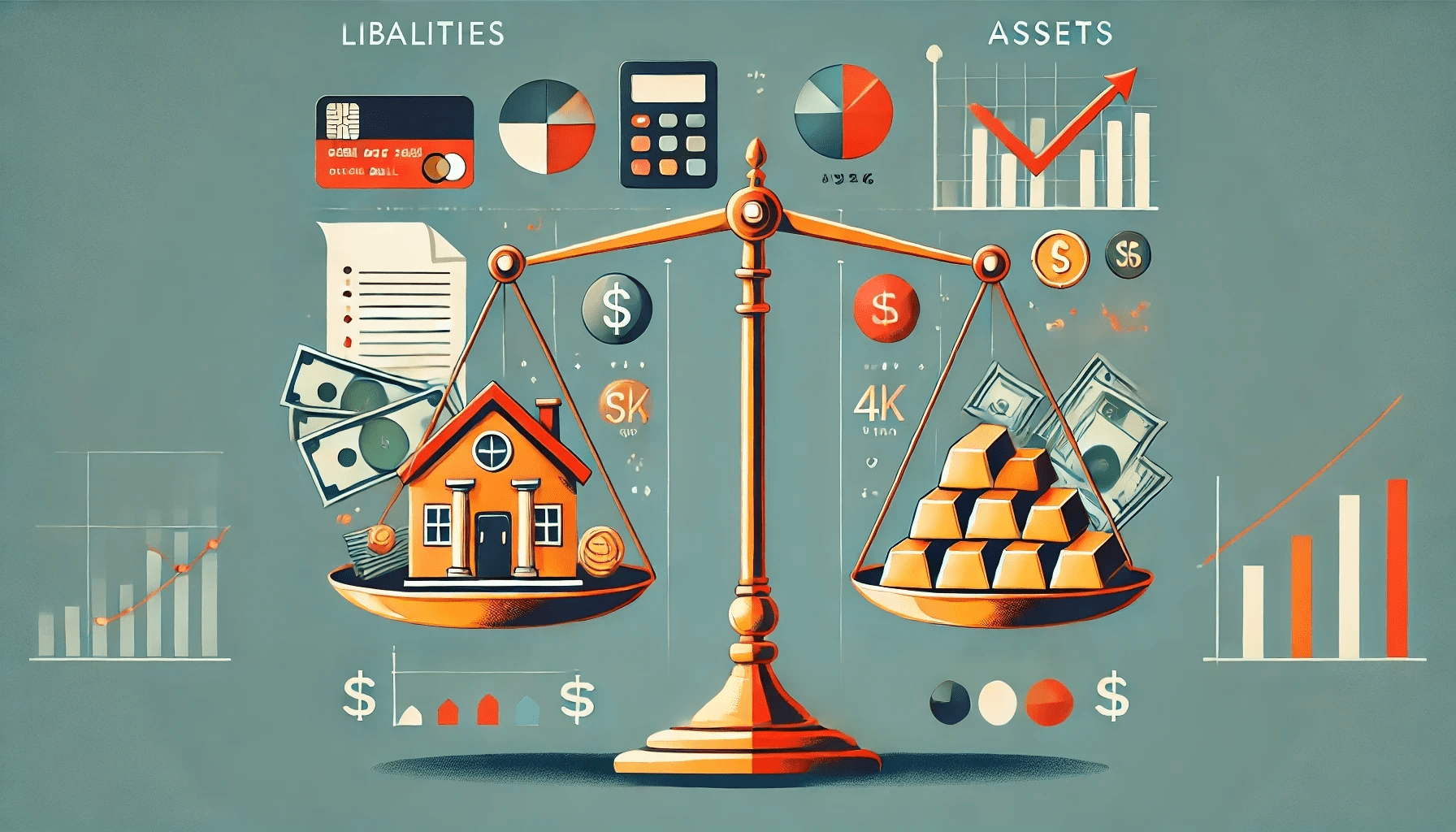

Overview of How Assets and Liabilities Shape Financial Success.

Understanding assets and liabilities is key to wealth. Assets put money in your pocket—things like investments, rental properties, and businesses. Liabilities take money out, like car payments, credit card debt, and loans.

Millionaires focus on buying assets that grow in value. They avoid unnecessary liabilities that drain their income. This helps them build wealth instead of struggling to keep up with expenses.

A Millionaire Mindset means making smart money choices. Instead of spending on things that don’t bring long-term value, invest in assets that grow your wealth. The more assets you own, the closer you get to financial freedom.

What is the Millionaire Mindset?

Millionaires See Opportunities Where Others See Risks.

A Millionaire Mindset is all about perspective. While most people hesitate when faced with challenges, millionaires see them as chances to grow. They understand that every risk, when carefully planned, can open doors to new financial opportunities. Instead of backing away from uncertainty, they look for ways to turn it into success.

Rather than fearing failure, they see mistakes as valuable lessons. Every setback teaches them something new. Instead of avoiding tough situations, they find ways to learn, adjust, and move forward stronger than before.

This shift in thinking makes a big difference. Instead of saying, “What if I lose money?” millionaires ask, “What if this investment changes my future?” They train themselves to recognize possibilities, even when the outcome isn’t certain. With smart planning and the right mindset, they take strategic action and build lasting success.

They Focus on Long Term Growth Rather Than Short-Term Gratification.

People with a Millionaire Mindset always think ahead. Instead of looking for quick wins or spending money on temporary pleasures, they focus on building wealth that lasts a lifetime. They understand that small sacrifices today can lead to big rewards in the future.

While many people spend their money on things that lose value, millionaires make smarter choices. They invest in assets like real estate, stocks, and businesses… These things that grow over time. This allows them to build financial stability and create wealth that works for them.

This long-term thinking leads to greater security. By making smart choices today, they set themselves up for success down the road. They know that patience and discipline pay off and that real wealth comes from smart planning, not impulse decisions.

Investing in Knowledge, Skills, and Smart Decisions.

A Millionaire Mindset prioritizes learning. Wealthy people understand that knowledge is one of the most valuable investments they can make. Instead of relying on luck, they educate themselves. They read books, take courses, and learn from mentors who push them to grow.

They also invest in developing skills that increase their earning potential. Whether it’s understanding business strategies, improving financial literacy, or mastering a new trade, they focus on continuous learning. These skills help them make smarter financial choices and avoid costly mistakes.

By making informed decisions, they reduce risk. Instead of guessing or acting on emotions, millionaires rely on research and data. They know that every financial move, big or small, affects their long term success. By staying informed, they build a solid foundation for wealth.

The Importance of Financial Discipline and Continuous Improvement.

Discipline is the foundation of a Millionaire Mindset. Successful individuals know that wealth isn’t built overnight. It takes consistent, smart decisions over time. That’s why they avoid unnecessary spending and stick to a financial plan that supports their long term goals.

They also believe in constant improvement. They track their progress, make adjustments, and learn from past mistakes. Instead of staying in their comfort zone, they challenge themselves to grow. This habit keeps them ahead in business, investments, and personal finance.

Success isn’t about a single big win! It is about the small, smart choices made every day. Millionaires stay committed to learning, improving, and refining their financial habits. They know that true wealth comes from patience, persistence, and making the right decisions over time.

Understanding Assets: What Builds Wealth?

Assets Put Money in Your Pocket! Examples Include Real Estate, Stocks, and Businesses…

A Millionaire Mindset focuses on building assets because they create long-term wealth. Unlike liabilities, which take money away, assets bring in income and grow in value over time. Real estate, stocks, and businesses are some of the best assets to invest in.

Real estate makes money through rent and property value increases. Stocks grow wealth through dividends and long term gains. Owning a business can provide both regular income and passive profits, making it one of the best ways to build financial freedom.

Millionaires don’t just work for money! They let money work for them. The more income generating assets they own, the faster their wealth grows. This shift in thinking helps them escape paycheck dependency and build lasting financial security.

Passive Income versus Active Income and Why Assets Matter.

Not all income is the same. Most people rely on active income, which requires constant effort. They trade time for money, meaning their income stops if they stop working. A Millionaire, however, focuses on passive income. Passive money that keeps coming in even when they aren’t working.

Passive income comes from assets like rental properties, dividend-paying stocks, and automated businesses. These income streams require little ongoing effort. Over time, passive income allows millionaires to enjoy financial freedom and more control over their time.

Building passive income takes time, but the rewards are worth it. While active income covers daily expenses, passive income builds long-term wealth. The goal is to stop working for money and start making money work for you.

Cash Flow versus Capital Gains. Understanding How Assets Generate Wealth.

Wealth-building depends on two things: cash flow and capital gains. Cash flow is the steady income from assets, like rental payments or stock dividends. Capital gains happen when an asset increases in value over time, like when a house or stock becomes worth more.

Millionaires aim for both. Cash flow provides regular income that can be reinvested, while capital gains build wealth over time. This combination ensures financial stability and continued growth.

Focusing only on capital gains can be risky since market values rise and fall. Strong cash flow, however, provides consistent income even in tough times. A Millionaire balances both, creating multiple streams of wealth.

The Importance of Asset Diversity for Financial Stability.

A Millionaire never depends on just one type of investment. Spreading money across different assets reduces risk and increases financial security. If one investment struggles, others can still bring in income.

For example, if the stock market drops, rental income from real estate can provide stability. If property values decline, business profits or stock dividends can keep cash flowing. This strategy ensures steady income no matter what happens in the economy.

Diversification also opens new opportunities for growth. Instead of relying on a single investment, smart investors spread their money across different industries and income streams. This approach builds long-term wealth and financial security.

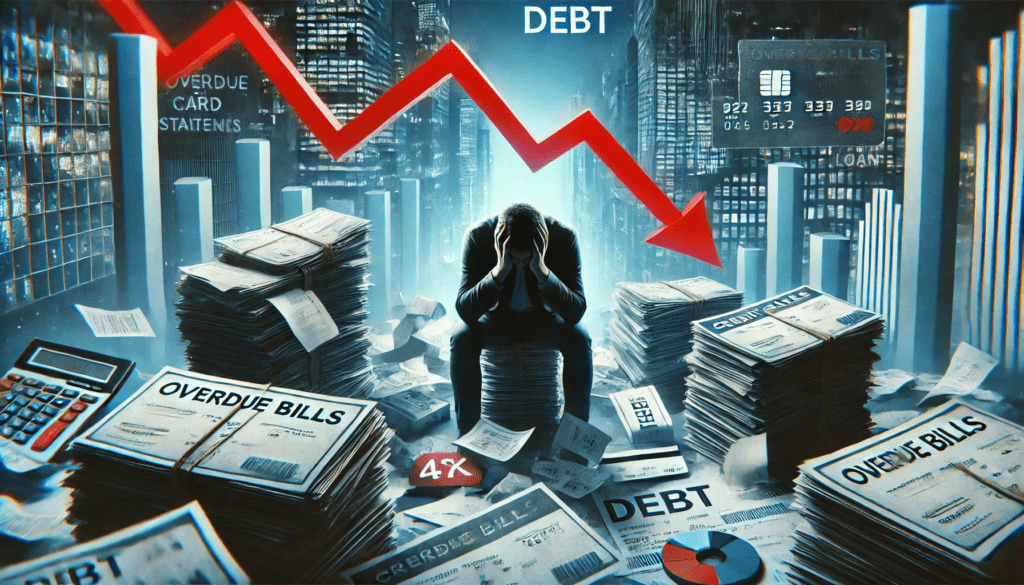

Understanding Liabilities: What Holds You Back?

Liabilities Take Money Out of Your Pocket! Examples Include Debt, Luxury Expenses, and High-Interest Loans.

A Millionaire focuses on building wealth, but liabilities do the opposite. Liabilities take money away, making it harder to grow financially. Common examples include debt, luxury purchases, and high-interest loans.

Buying expensive items may feel good, but they don’t help in the long run. A new car loses value as soon as you drive it. Credit card debt keeps you stuck with monthly payments and high interest. These expenses make it harder to save and invest.

To build wealth, it is important to avoid unnecessary liabilities. Millionaires keep expenses low and focus on buying assets instead. The less money wasted on liabilities, the more money they have to grow their wealth.

The Difference Between Good Debt and Bad Debt.

Not all debt is bad. A Millionaire Mindset separates debt into two types: good debt and bad debt. Knowing the difference helps people make smarter financial choices.

Good debt helps build wealth. A mortgage on a rental property can bring in rental income. A business loan can help a company grow and make more profit. This type of debt pays for itself over time.

Bad debt, however, drains your money. Credit cards, payday loans, and car payments often come with high interest. These debts take money without adding financial value. Smart investors avoid bad debt and use good debt to grow their wealth.

How Overspending on Liabilities Keeps People Trapped in the Rat Race.

Many people struggle financially because they spend too much on liabilities. Instead of investing, they buy things that lose value. This keeps them living paycheck to paycheck. A Millionaire Mindset focuses on breaking this cycle.

The more money spent on unnecessary expenses, the harder it is to save. If income goes straight to paying off credit cards, car loans, or luxury items, there’s little left to invest. This keeps people stuck working endlessly without building wealth.

To escape the rat race, spending habits must change. Millionaires avoid wasting money on things that don’t grow in value. Instead, they invest in assets that increase their financial security over time.

Smart Ways to Reduce Liabilities and Free Up Cash Flow.

A Millionaire Mindset focuses on reducing liabilities and freeing up cash for investing. The first step is cutting unnecessary expenses. Avoiding luxury items, high-interest debt, and impulse spending helps save more money.

Another key strategy is paying off bad debt quickly. High-interest loans and credit cards drain money every month. Getting rid of these debts frees up cash that can be used to build wealth instead.

Finally, smart financial planning helps avoid new liabilities. Living within your means, making thoughtful purchases, and choosing investments over unnecessary spending lead to long-term success. The less money wasted on liabilities, the more wealth you can build.

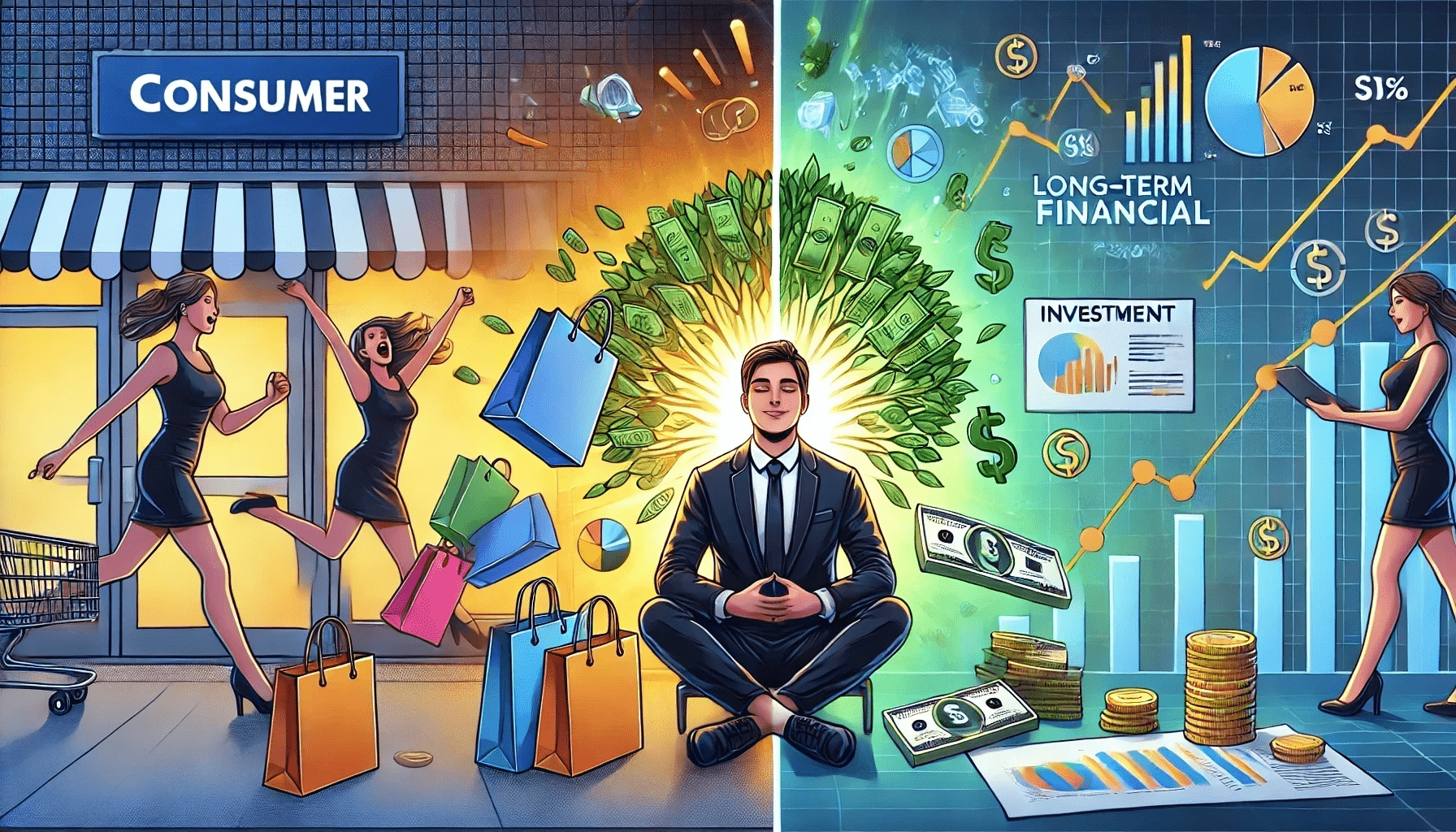

Shifting from Consumer to Investor Mindset!

A Millionaire Mindset Focuses on Acquiring Income Producing Assets Instead of Luxury Items.

A Millionaire Mindset is all about smart money choices. Instead of spending on expensive cars, designer clothes, or the latest gadgets, millionaires put their money into assets that grow in value. They know that real financial security comes from owning things that generate income.

Assets like rental properties, dividend-paying stocks, and businesses provide steady cash flow. These investments work for them, creating wealth without needing constant effort. The more income-producing assets they collect, the faster they build financial freedom.

Luxury items bring short term happiness, but they don’t create lasting wealth. Millionaires plan for the future. They focus on building net worth by putting their money into things that will increase in value and provide financial stability.

A Millionaire Mindset Uses Delayed Gratification: Why Investing Comes Before Spending.

A Millionaire Mindset means choosing patience over impulse spending. Many people spend money as soon as they earn it, chasing short-term pleasures. Millionaires, however, invest first and spend later.

They know that money grows when placed in the right investments. Every dollar they invest today has the potential to multiply over time. Instead of buying expensive items now, they let their investments create more wealth. Later, they can afford luxuries without harming their financial future.

This self discipline leads to long-term success. Millionaires build financial security by putting investments before spending. They understand that smart money choices today lead to bigger rewards in the future.

A Millionaire Mindset Builds Wealth by Reinvesting Profits.

A Millionaire is not just about making money! They are about growing money. Successful people don’t spend all their profits. Instead, they reinvest earnings to create even more wealth.

For example, a business owner reinvests profits to expand, leading to higher revenue. An investor uses stock dividends to buy more shares, increasing future payouts. This reinvestment cycle creates compounding growth, multiplying wealth over time.

This habit sets millionaires apart. Instead of cashing out early, they let their money work for them. By reinvesting profits, they create a financial system that continues to grow with minimal effort.

A Millionaire Mindset Starts with Daily Financial Habits.

A Millionaire Mindset is built through small, smart financial decisions. Daily habits shape long-term success. Millionaires create routines that align with their financial goals, making steady progress toward wealth.

They track expenses, avoid unnecessary debt, and make thoughtful spending choices. Instead of wasting money, they invest in assets, save for the future, and focus on self-improvement. These small daily actions add up over time.

Success doesn’t happen overnight. It comes from making smart choices every day. By sticking to good financial habits and staying focused on long-term goals, millionaires continue to grow their wealth year after year.

The Role of Passive Income in Wealth Building.

Why Passive Income is Key to Financial Freedom with a Millionaire Mindset.

A Millionaire Mindset understands that financial freedom comes from making money work for you. If you only rely on a paycheck, your earning potential is limited. But with passive income, you can earn money even when you’re not working. This gives you more financial security and control over your time.

With passive income, you don’t have to trade hours for dollars. Instead, money flows in from investments, rental properties, or automated businesses. The more income streams you build, the closer you get to financial independence. Wealthy people use this strategy to secure long-term wealth and create financial stability.

Financial freedom means covering your expenses without depending on a job. Passive income makes this possible. A Millionaire Mindset focuses on creating these income streams to live life on their own terms, without financial stress.

Examples of Passive Income Streams.

A Millionaire Mindset finds ways to make money with little ongoing effort. Some of the best passive income streams include dividends, rental properties, royalties, and business automation. These investments keep earning money even when you aren’t actively working on them.

Dividends come from stocks that pay investors regularly. Rental properties bring in steady income from tenants. Royalties provide long-term earnings from books, music, or patents. Automated businesses, like e-commerce stores or digital courses, generate money without daily involvement.

Having multiple income streams increases financial security. Millionaires don’t depend on just one source of income. Instead, they spread their investments across different areas. This way, they continue earning money even if the economy shifts.

How to Shift from an Earned Income Mindset to a Passive Income Strategy.

To go from working for money to letting money work for you, you need a Millionaire Mindset. Most people believe they must trade time for income, but the key to financial freedom is focusing on investments that generate steady earnings.

Start by saving and investing. Instead of spending your entire paycheck, put money into assets like stocks, real estate, or online businesses. Even small investments can grow into reliable income streams over time.

Next, reinvest your profits. Instead of spending dividends or rental earnings, use them to buy more assets. A Millionaire Mindset understands that compounding earnings can grow wealth much faster, leading to long-term financial security.

The Power of Compounding and Reinvesting Passive Income.

A Millionaire Mindset doesn’t just earn money! It multiplies it! One of the most powerful ways to build wealth is by reinvesting passive income. This allows money to grow on its own through the power of compounding.

For example, dividends from stocks can be reinvested to buy more shares, increasing future payouts. Rental income can be used to purchase more properties, creating even more cash flow. Profits from automated businesses can be reinvested in marketing or expansion to grow revenue.

Long-term wealth comes from making money work for you. A Millionaire Mindset reinvests passive income instead of spending it. This strategy speeds up financial growth and leads to true financial independence.

Millionaire Success Habits… Daily Routines That Lead to Wealth!

Millionaire Mindset and the Importance of Setting Clear Financial Goals.

A Millionaire Mindset starts with a clear financial plan. Without goals, it’s easy to lose focus and make little progress. Setting specific financial targets creates a roadmap to success. Whether it’s saving money, paying off debt, or increasing income, having a plan keeps you on track.

Checking your progress is just as important as setting goals. Reviewing finances regularly helps you see what’s working and what needs to change. Many millionaires track their financial progress weekly or monthly to stay on the right path.

Small steps lead to big results over time. Adjusting goals along the way keeps you moving forward. A Millionaire Mindset knows that wealth is built through smart, consistent actions, not overnight success.

Millionaire Mindset Focuses on Continuous Learning.

A Millionaire Mindset values education beyond school. The most successful people never stop learning. They read books, attend seminars, and seek advice from experts. Learning more about money helps them make better decisions and avoid costly mistakes.

Reading about investing, business, and finance gives fresh ideas. Learning from others’ experiences saves time and helps avoid common money traps. Many successful people also listen to podcasts, watch financial videos, and follow market trends.

Mentorship speeds up success. Millionaires surround themselves with people who have already achieved financial growth. Learning from experts makes it easier to make smarter money choices and grow wealth faster.

Millionaire Mindset Thrives in the Right Environment.

The people around you shape your mindset. A Millionaire Mindset means surrounding yourself with positive, motivated people. Being around successful individuals pushes you to think bigger and do better.

Negative people can slow you down. Those who complain about money or lack ambition can hold you back. Millionaires connect with people who support their goals and challenge them to improve.

Success happens faster in the right environment. Networking with successful people opens doors to business deals, investment ideas, and new opportunities. A Millionaire understands the power of relationships and builds connections that lead to success.

Millionaire Mindset Takes Smart Risks and Learns from Failure.

A Millionaire is not afraid to take smart risks. Playing it safe all the time can limit financial growth. Millionaires weigh the risks and rewards before making decisions.

Failure is part of the journey. Instead of fearing mistakes, wealthy individuals learn from them. Every failure teaches a lesson that helps refine future strategies. The most successful people see setbacks as learning opportunities, not obstacles.

Risk creates new possibilities. Investing, starting a business, or entering new markets all come with uncertainty. A Millionaire prepares for challenges, learns from them, and turns them into financial success.

How to Leverage Debt and Credit Wisely.

Millionaire Mindset Understands Good Debt Versus Bad Debt.

Not all debt is bad. A Millionaire knows the difference between good debt, which builds wealth, and bad debt, which takes money away. Borrowing to invest in income producing assets is smart. Borrowing for luxury purchases is a financial mistake.

Good debt includes loans for rental properties, business growth, or education that increases income. These investments pay for themselves over time. Bad debt, like high interest credit cards, car loans, and unnecessary personal loans, does not bring financial returns.

Using debt wisely helps build wealth. Avoiding bad debt keeps financial stress low. A Millionaire Mindset uses borrowed money strategically to create growth, not financial trouble.

Millionaire Mindset Uses Credit to Buy High Value Assets.

Millionaires don’t use credit for things that lose value. They use it to buy assets that make money. A Millionaire Mindset sees credit as a tool to grow wealth, not to fund a lifestyle.

Millionaires take mortgages to buy rental properties that generate cash flow. They will use business loans to expand and increase profits. A millionaire invest borrowed money in assets that provide long-term financial benefits.

Using credit wisely means focusing on investments that grow in value. Millionaires avoid using debt for personal expenses that don’t pay them back. A Millionaire chooses financial growth over short term rewards.

Millionaire Mindset Builds and Protects Strong Credit Scores.

A strong credit score creates financial opportunities. A Millionaire Mindset understands that good credit leads to lower interest rates, better loans, and more buying power. Managing credit well is key to building wealth.

Paying bills on time is the most important step. Keeping credit card balances low and not maxing out available credit also helps. Checking credit reports regularly prevents errors and fraud.

Millionaires use credit carefully. They don’t over borrow or take unnecessary risks. They protect their credit scores to keep financial options open. A Millionaire treats credit as an asset, not a burden.

Millionaire Mindset Uses Debt to Build Wealth, Not Create Burden.

Debt can be a powerful tool when used correctly. A Millionaire sees debt as leverage, not as a financial trap. Borrowing wisely can speed up wealth-building.

Smart investors use debt to buy appreciating assets. Real estate investors take mortgages to acquire rental properties. Business owners use loans to grow profits and scale operations.

Irresponsible borrowing leads to financial stress. Using debt wisely ensures it works in your favor. A Millionaire Mindset focuses on credit as a tool for success while avoiding unnecessary risks.

Building Generational Wealth Through Smart Investments.

A Millionaire Knows Wealth Is More Than Just Making Money!

Wealth isn’t just about earning a big paycheck. A Millionaire Mindset understands that keeping and growing money is just as important. Many people make good money but still struggle because they do not manage it wisely.

Saving and investing are key to building wealth. Without a plan, money can disappear quickly. Wealthy individuals focus on increasing their net worth, not just their income. They avoid unnecessary spending and put money into assets that grow over time.

Smart money management leads to long-term financial success. A Millionaire Mindset protects and multiplies wealth. The goal isn’t just to make money, it is to create lasting financial security.

Investing in Real Estate, Stocks, and Businesses for Stability.

Financial stability comes from owning assets. Instead of relying on a single income source, wealthy individuals invest in real estate, stocks, and businesses. These investments provide long-term security and steady cash flow.

Real estate generates rental income and increases in value. Stocks provide dividends and long-term financial growth. Owning a business allows for greater control over income and expansion. Each of these assets plays a key role in financial independence.

Diversifying investments reduces risk. Smart investors don’t put all their money into one type of asset. By spreading money across multiple investments, they ensure steady financial growth, even if one market slows down.

Growing and Protecting Wealth Over Time.

Making smart investments is only part of building financial security. Wealth must also be protected and reinvested. Keeping money in a savings account is not enough. It needs to be put to work.

Reinvesting profits helps money grow faster. Instead of spending earnings from investments, successful people use them to buy more assets. They expand real estate holdings, reinvest stock dividends, and grow their businesses.

Long term success requires planning. Wealth building isn’t just about today, it is about making financial decisions that create stability for years to come. The right strategies ensure money continues to grow.

Building Wealth That Lasts for Generations.

Successful families don’t just build wealth, they pass it down. Financial knowledge and estate planning help preserve money for future generations. Without a plan, wealth can disappear in just a few decades.

Trusts, long-term investments, and financial education play a key role. Teaching younger generations how to manage money ensures they continue to grow wealth rather than spend it carelessly. Discipline and smart decisions keep wealth alive.

A lasting legacy is built through smart investments and financial education. Families that focus on growth and preservation create financial security that continues for generations.

Overcoming Financial Mistakes and Learning from Setbacks.

Millionaire Mindset Avoids Common Financial Mistakes.

Many people struggle with money because they repeat the same mistakes. A Millionaire Mindset learns from these errors and makes better choices. One major mistake is spending more than you earn. Overspending leads to debt, which slows down financial growth.

Another mistake is waiting too long to invest. Many people delay saving and miss out on compound interest. Successful individuals start early, even with small amounts. Investing regularly builds financial security over time.

Ignoring financial education also holds people back. Many never take the time to learn about money management or investing. A Millionaire Mindset values financial knowledge and applies it to make smart, long-term decisions.

Staying Persistent and Resilient While Building Wealth.

Wealth takes time to grow. Many people give up too soon because they want quick results. A Millionaire Mindset understands that success is a long-term process. Staying consistent, even during slow progress, is key.

Challenges will come. Market downturns, surprise expenses, and failed investments happen. But resilience separates those who succeed from those who quit. Instead of fearing obstacles, they use them as learning experiences.

Adapting is essential. The economy changes, business trends shift, and new opportunities arise. Those who adjust their strategies and keep moving forward stay on track. A Millionaire Mindset remains focused, no matter the challenges.

Bouncing Back and Moving Toward Financial Freedom.

Financial setbacks happen to everyone. Losing money in investments, dealing with debt, or facing unexpected expenses can feel overwhelming. A Millionaire Mindset does not dwell on failure but looks for solutions.

The first step is understanding what went wrong. Learning from mistakes prevents them from happening again. A solid financial plan turns setbacks into temporary obstacles, not permanent roadblocks.

Taking action is key. Cutting unnecessary spending, earning more, or restructuring debt helps rebuild financial stability. Staying committed to long term goals turns setbacks into stepping stones. A Millionaire Mindset sees every challenge as a chance to grow and move closer to financial freedom.

Taking Action and Applying the Millionaire Mindset.

Wealth-building is a long-term process, not a quick fix. A Millionaire focuses on patience and discipline to create lasting financial success. Rushing into risky investments or expecting overnight results often leads to failure. Instead, steady progress and smart decisions lead to real financial freedom.

Every financial move should support long term goals. Saving, investing, and avoiding unnecessary debt are key. Those who stay consistent and stick to their financial plan will see results. A Millionaire Mindset knows that small efforts today turn into big rewards in the future.

The best way to grow wealth is to start today. Small, consistent actions lead to big financial improvements over time. A Millionaire focuses on daily habits like saving a portion of income, budgeting wisely, and avoiding impulse spending.

It’s easy to feel like small steps don’t matter, but they do. Every dollar saved and invested adds up. Over time, these small efforts create financial stability and independence. A Millionaire treats every financial decision as a step toward long-term success.

Building wealth means owning assets, not accumulating debt. A Millionaire Mindset prioritizes investments in real estate, stocks, and businesses. These income-generating assets increase in value and provide long-term security.

At the same time, reducing liabilities is just as important. High-interest debt, unnecessary expenses, and poor money choices drain financial resources. The less money wasted, the more can be used for wealth-building. A Millionaire balances earning, saving, and investing to create a strong financial future.

Conclusion!

True wealth starts with changing how you think about money. A Millionaire Mindset commits to making smart financial choices and staying focused on long-term success. Financial freedom doesn’t come from luck, it comes from strategic planning and disciplined habits.

Instead of chasing quick money, focus on stability and growth. Learn about investing, avoid reckless spending, and take control of your finances. A Millionaire Mindset understands that every choice today shapes the future. The path to wealth starts with commitment and a smart financial plan.

Social Media Accounts To Follow!

About us!

One Key To Success Is an Online Presence Click Here And Start Creating Websites!